How Much House Can I Afford in Dallas in 2026?

The amount of house you can afford in Dallas in 2026 depends less on a simple income multiple and more on the total monthly payment you can comfortably carry.

Your mortgage principal and interest are only part of that payment. Dallas buyers also need to account for property taxes, homeowners’ insurance, mortgage insurance when applicable, HOA dues, utilities, maintenance, and the cash required at closing.

A lender may approve you for more than you want to spend. The better question is not only, “How much can I qualify for?” It is, “What purchase price lets me own a home while continuing to save, travel, handle repairs, and live comfortably?”

Start With a Comfortable Monthly Payment

Before choosing a home price, decide what you want your total monthly housing expense to be.

That number should include:

Mortgage principal and interest

Property taxes

Homeowners insurance

Private mortgage insurance, if required

HOA dues, if applicable

A reasonable allowance for maintenance

For example, two Dallas homes with the same purchase price can have noticeably different monthly costs. One may be in a neighborhood with higher property taxes or an HOA. Another may be older and require a larger maintenance reserve.

This is why affordability should be calculated property by property, not only from the list price.

What Mortgage Rates Mean for Dallas Buyers in 2026

As of June 11, 2026, Freddie Mac reported an average rate of 6.52 percent for a 30-year fixed-rate mortgage. That national average is a useful reference point, but your actual rate will depend on your credit profile, loan program, down payment, debt, occupancy, and lender.

At approximately 6.52 percent, every $100,000 borrowed costs about $633 per month in principal and interest on a 30-year loan. That does not include taxes, insurance, mortgage insurance, or HOA fees.

A relatively small change in your interest rate can affect your buying power. Rather than trying to predict exactly where rates will go, ask a lender to calculate several realistic scenarios. You can then compare what happens at different rates, down payments, and purchase prices.

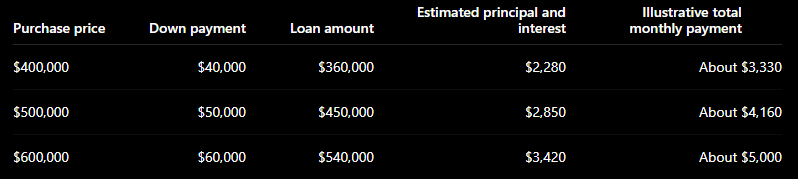

Estimated Monthly Payments at Different Dallas Home Prices

The following examples use a 30-year fixed mortgage at 6.52 percent with 10 percent down.

For illustration, the estimates also assume annual property taxes equal to approximately 2.2 percent of the purchase price, homeowners’ insurance equal to approximately 0.5 percent, and private mortgage insurance equal to approximately 0.5 percent of the loan balance. Actual expenses can vary considerably by property, insurance history, exemptions, lender, and loan program.

These totals do not include HOA dues, utilities, repairs, or optional services. They are not loan quotes, but they demonstrate why the full payment matters more than the mortgage amount alone.

A buyer who feels comfortable spending $3,300 per month may be looking for a home near $400,000 under these assumptions. A buyer comfortable with $5,000 per month may be closer to $600,000.

Changing the down payment, interest rate, tax rate, or insurance premium will change those numbers.

How Much Income Do You Need to Buy a House in Dallas?

There is no single income requirement because buyers have different debts and financial profiles.

Lenders evaluate your debt-to-income ratio, commonly called DTI. This compares your monthly debt obligations with your gross monthly income. Car payments, credit cards, student loans, personal loans, and the proposed housing payment may all affect the calculation.

Consider two households earning the same income:

One has no car payment, minimal credit card debt, and a large cash reserve. The other has two car payments, student loans, and higher recurring obligations. Even with identical salaries, their comfortable home budgets may differ significantly.

Student loan debt does not automatically prevent someone from becoming a homeowner. Our guide to buying a home in Dallas with student loan debt explains how lenders consider those monthly obligations within the broader financial picture.

Your lender will determine what you can qualify for. Your personal budget determines what you should spend.

You May Not Need a 20 Percent Down Payment

Many Dallas buyers assume they need to save 20 percent before purchasing a home. That is not always the case.

Depending on eligibility, conventional financing may allow a qualified borrower to purchase with a smaller down payment. FHA financing may also provide a lower down-payment option. VA-eligible borrowers may have access to financing without a required down payment, subject to loan approval and program requirements.

A smaller down payment can allow you to purchase sooner, but it may increase the loan balance and monthly payment. It may also result in mortgage insurance.

A larger down payment can reduce your payment and create more equity at closing, but putting every available dollar into the home may leave you without enough cash for repairs, furnishings, emergencies, or plans.

For buyers considering Lakewood, the M Streets, Lake Highlands, Forest Hills, or surrounding neighborhoods, our article on buying a home in East Dallas without a huge down payment discusses how financing and neighborhood strategy can work together.

Do Not Forget Closing Costs and Cash Reserves

Your down payment is not the only cash you may need.

Buyer closing expenses can include lender fees, appraisal charges, title-related costs, prepaid homeowners insurance, prepaid interest, and initial property tax or escrow deposits. The amount depends on the transaction and loan structure.

You should also consider:

Inspection and due diligence costs. Buyers commonly pay for inspections and other property evaluations before closing.

Moving and immediate improvements. Even a well-maintained home may need paint, appliances, window treatments, landscaping, or furniture.

Emergency reserves. Homeownership is easier when an unexpected plumbing issue or HVAC repair does not create financial stress.

Appraisal-related cash. In a competitive situation, an appraisal may come in below the contract price. Depending on the contract and negotiations, the buyer may need additional cash or another solution. Our guide to what happens when a Dallas home appraisal comes in low explains the available options.

The goal is not to arrive at closing with the smallest possible bank balance. A thoughtful purchase leaves room for life after closing.

The 2026 Conforming Loan Limit in Dallas

For 2026, the baseline conforming loan limit for a one-unit property is $832,750. A loan above the applicable conforming limit is generally considered a jumbo loan and may involve different qualification, reserve, credit, and down-payment requirements.

The loan limit is not the same as the purchase-price limit.

For example, someone purchasing a home above $832,750 may still use conforming financing if the down payment keeps the loan amount at or below the applicable limit. A lender can compare conforming and jumbo structures to determine which approach is more favorable.

This distinction is particularly relevant in Highland Park, University Park, Preston Hollow, Bluffview, Devonshire, and higher-priced parts of Lakewood, where many homes may require buyers to consider jumbo financing or a larger down payment.

Where Your Budget May Fit in Dallas

Dallas is not one uniform housing market. Affordability can change from one neighborhood to another and sometimes from one street to the next.

Lakewood and the M Streets

Buyers are often drawn to these areas for their architecture, established streets, central location, and proximity to White Rock Lake, Lower Greenville, and East Dallas amenities.

Pricing can vary substantially based on lot location, renovation quality, home size, school attendance zones, and proximity to major roads. Buyers may need to choose among square footage, updates, lot size, and location within the neighborhood.

Lake Highlands

Lake Highlands offers a wide range of homes, from smaller traditional properties to larger renovated residences. Because the area covers several distinct pockets, buyers may find different opportunities depending on the subdivision, school attendance zone, home condition, and proximity to parks or trails.

Casa Linda and Forest Hills

These East Dallas neighborhoods can appeal to buyers looking for larger lots, mature trees, and convenient access to White Rock Lake and the Dallas Arboretum area. Inventory and property conditions vary, making local pricing analysis especially important.

Devonshire and Bluffview

Devonshire and Bluffview often attract buyers looking for central locations, architectural variety, established surroundings, and proximity to areas such as Inwood Village and the Dallas North Tollway.

Lot value, renovation quality, and redevelopment activity can create meaningful price differences between nearby properties.

Highland Park, University Park, and Preston Hollow

Buyers in the Park Cities and Preston Hollow are often shopping in higher price ranges, but affordability still depends on more than the purchase price. Property taxes, insurance, maintenance, remodeling plans, and jumbo loan requirements can materially affect the budget.

Competition may also remain strong for well-positioned homes. Our guide to buying in Preston Hollow or the Park Cities when competition is intense explains how preparation and offer structure can make a difference.

You can also visit the Mysti Stewart Group’s Dallas neighborhoods page to compare communities and begin narrowing your search.

How to Calculate a Realistic Dallas Home Budget

Begin with your monthly comfort level rather than a maximum approval amount.

Ask a lender to prepare estimates at several purchase prices. Each estimate should include the projected mortgage payment, property taxes, homeowners’ insurance, mortgage insurance, and HOA dues when applicable.

Then stress-test the budget.

Would the payment still feel comfortable after an insurance increase? Could you manage a major home repair? Would you still be able to contribute to savings and retirement? Does the budget leave room for childcare, travel, tuition, or other priorities?

It is also helpful to compare actual properties. A $550,000 home with lower taxes and no HOA may cost less each month than a $525,000 home with higher taxes, an HOA, and more expensive insurance.

Once you have a comfortable payment range, a Dallas Realtor can help identify neighborhoods and property types that align with it.

Should You Buy at the Top of Your Approval Range?

Not necessarily.

Lender approval is based on underwriting standards. It does not fully account for every personal expense or lifestyle goal.

You may prefer to stay below your maximum when:

Your income includes commissions, bonuses, or variable compensation

You expect childcare, tuition, or medical expenses to increase

You plan to renovate after purchasing

You own a business or have fluctuating income

You want to maintain a substantial emergency fund

You value travel, investing, or flexibility more than additional square footage

Buying below your maximum can also give you more room to handle rising taxes, insurance, maintenance, and utility costs.

The right house is not simply the most expensive one you can purchase. It is the home that fits your life without making the rest of your financial goals feel fragile.

Why Work with Mysti Stewart and the Mysti Stewart Group?

Affordability in Dallas is both a financial question and a neighborhood question.

A lender can explain how much you qualify to borrow. The Mysti Stewart Group helps you understand what that budget can realistically purchase across Lakewood, East Dallas, the M Streets, Lake Highlands, Highland Park, University Park, Preston Hollow, Devonshire, Bluffview, Forest Hills, Casa Linda, and surrounding Dallas neighborhoods.

That guidance includes comparing neighborhood price points, evaluating property taxes and HOA expenses, identifying homes that may require immediate work, analyzing comparable sales, and structuring an offer that protects your broader financial goals.

With deep Dallas market knowledge and nearly 50 years of combined team experience, the Mysti Stewart Group helps buyers look beyond the approval letter and make decisions that feel sustainable long after closing.

Final Thoughts

How much house can you afford in Dallas in 2026?

The answer is the purchase price that creates a manageable total monthly payment, preserves enough cash for closing and homeownership, and supports your long-term plans.

Start with a trusted lender, calculate the full payment rather than principal and interest alone, and compare actual neighborhood costs before setting your search range. A careful budget may reveal that you can comfortably afford more than expected, or that staying below your approval amount gives you the lifestyle and flexibility you value most.

When financing and neighborhood strategy are considered together, the Dallas home search becomes much clearer.

Frequently Asked Questions

1. How much house can I afford in Dallas with a $100,000 salary?

It depends on your down payment, interest rate, property taxes, insurance, credit, and existing monthly debt. Two buyers earning $100,000 may qualify for different amounts because their car payments, student loans, credit card balances, and cash reserves differ. A lender should calculate a personalized range, while you decide which payment fits comfortably within your lifestyle.

2. Is a 20 percent down payment required to buy a home in Dallas?

No. Qualified buyers may have conventional, FHA, VA, or other financing options that require less than 20 percent down. A lower down payment may result in a larger monthly payment or mortgage insurance, so compare the complete cost of each option.

3. How much should I budget for property taxes in Dallas?

Property taxes vary by location, taxing jurisdiction, exemptions, and assessed value. Do not rely only on the seller’s current tax bill because exemptions or valuation changes may affect what you pay after purchasing. Ask your lender and Realtor to estimate taxes for the specific property.

4. Should I get prequalified or preapproved before looking at Dallas homes?

A thorough preapproval is generally more useful than a basic prequalification. It can clarify your financing, payment range, cash requirements, and potential loan conditions before you begin making offers. In competitive Dallas neighborhoods, strong financing preparation can also help an offer appear more dependable.

5. Can I afford a more expensive home if mortgage rates decline later?

A lower rate may increase buying power, but home prices and competition can also change when rates decline. Buy based on a payment you can manage at the time of purchase, rather than assuming a future refinance. Refinancing may become an option later, but it is never guaranteed.